Proprietorship Section Entries

- Admin4

- RPT Admin (Unlicensed)

General

In terms of section 7 of the Land Registration etc. (Scotland) Act 2012, the Keeper must enter in the proprietorship section of the title sheet:

- the name and designation of the proprietor, see Names and Changes of Name in the Proprietorship and Securities Sections and Designations

- in the case of common ownership the respective shares of the proprietor, see Common and Joint Ownership in the Proprietorship Section below.

In terms of section 10 of the Act, there is additional information that the Keeper must enter in the title sheet and some of this will fall to be entered in the proprietorship section, which would include:

- matters relating to warranty, see Warranty:

- particulars of any special destination, see Destinations

- reference to an entry in the Register of Inhibitions that might affect the validity of a deed being registered, see Insolvency - Personal and Corporate

- such other information as the Keeper considers appropriate (this will include the date of registration and consideration in terms of regulation 12(2) of the Rules), see below.

In rare cases, in addition to these requirements, a senior caseworker may authorise entries in the proprietorship section for:

- a statement under section 30(5) that the name or designation of the proprietor is not known or, as the case may be, is not known with reasonable certainty by the Keeper (but only in a title sheet being constituted under automatic plot registration or a Keeper-induced registration).

- On occasion, an alteration may be made to the proprietorship section when the registrable deed relates to another section of the title sheet. For example, a standard security by a new proprietor who has not completed their title by registration of a notice of title may be registered and an update to the proprietorship section is also appropriate to explain the entry for the standard security in the securities section - see Names and Changes of Name in the Proprietorship and Securities Sections.

Addition of Land to Title

Section 13(2)(a) of the 2012 Act gives the Keeper authority to combine cadastral units, e.g. on the acquisition of additional land. The following guidance is on the format of the proprietorship section; the property section will be amended by the plans officer who will map the subjects by the most convenient method, but the verbal description in the property section will describe the subjects as a whole unit.

The "date of first registration" noted in the property section will be the earliest date of registration of a part of the title. No further dates should be added when further areas are registered.

Acceptance of application

When adding subjects to an existing cadastral unit it is important to check that the proprietor holds title in the same capacity. For example if the existing title is held by A and B but the additional ground is only being acquired by A, then the cadastral units should not be combined. Similarly, where title is held under different destinations the cadastral units should not be combined.

Common and Joint Ownership in Proprietorship Section

Section 7(1)(b) and schedule 4, paragraph 11A(a) of the Act require that when property is held in common ownership, the respective shares of the proprietors whose right is registered must be entered in the proprietorship section of the title sheet.

There are two types of ownership of the same plot of land by more than one person: common ownership and joint ownership.

The registration officer should check that the pro indiviso shares in a proprietorship section will not, on the addition of the further share in the registrable deed which is under consideration, exceed one or 100%. If the shares would exceed one or 100%, the case should be referred to a senior caseworker for consideration.

Common Ownership

In common ownership, each of two or more proprietors has an absolute, unrestricted right to a fractional share of property and can dispose of or otherwise transact with their share.

The situation most likely to be encountered is ownership in equal shares, where the disposition specifies that the named disponees hold the property "equally between them". Entering this wording in the proprietorship section will comply with the requirement of the Act. Otherwise, the deed should indicate specifically the pro indiviso shares in which the property is held if it is not to be held by the proprietors in equal shares.

The following examples deal with dispositions which convey the whole plot of land to which a title sheet relates and not only a pro indiviso share. These examples would apply to both first registration and subsequent transmissions of the whole registered plot. Where the disposition or notice of title relates only to transmission of a pro indiviso share, see Pro Indiviso share of a whole unit of property below for more styles of entry.

Deed does not specify "equally between them" or fractional share

Registration officers may encounter a situation where the registrable deed conveys the property to more than one person but does not specify that they hold the property conveyed "equally between them" or in specified pro indiviso shares. As the Keeper is required to reflect the legal entitlement of each of the proprietors in terms of Section 7(1)(b) and schedule 4 paragraph 11A(a), the words "equally between them" should be added to the entry in the proprietorship section.

Pro indiviso share of a whole unit of property

Each proprietor may possess the whole property, subject to the rights of the other proprietors to share possession. Equally, each proprietor may transact with his share without consulting his co-owners – e.g. he may dispose of it, or burden it with debt – and on his death his share passes to his heirs or executors. Where it is not practical to transact with just one share in the property, any pro indiviso proprietor may apply to the court, either for the property to be physically divided (action of division), or more commonly for the whole property to be sold and the proceeds shared (action of division and sale).

Pro indiviso ownership can therefore be distinguished from:

- physical division of a property, where an identifiably separate part of the unit is disponed;

- rights of use (e.g. servitudes), where the whole ownership remains with a servient proprietor, who is burdened with the requirement to allow the dominant proprietor(s) to use the property for a specific purpose;

- joint ownership (e.g. title held by trustees), where one of the proprietors cannot deal with his interest separately from that of his co-proprietors.

At any one time, a significant proportion of the properties in Scotland will have some element of pro indiviso ownership in their titles. For instance, it occurs whenever a husband and wife take title equally between them. It also occurs when the ownership of (e.g.) a tenement flat carries with it a specified pro indiviso share or right of common ownership of a pertinent such as the drying green or the solum of the building.

The manner in which the Keeper will deal with an application for registration of a pro indiviso share will depend on whether:

- the application relates to a pro indiviso share of a whole unit of property; or

- the application relates to a pro indiviso share of a pertinent - see Shared and Sharing Plots Guidance and Shared and Sharing Plots

The remainder of this section deals only with pro indiviso shares of a whole unit of property.

Pro indiviso shares (Dealing with whole)

Where a person is registered as sole proprietor of an interest and subsequently transfers a pro indiviso share to someone else, when making entries in the proprietorship section, additional information regarding the various considerations is necessary. It is important that every proprietor is included to ensure that the terms of sections 7(1)(a) is complied with.

Similarly, where title is held by multiple parties and gradually transferred to one of them, clarification of the existing entries and consideration is necessary.

Pro indiviso shares (First Registration)

Where an application for first registration is induced by a disposition of a pro indiviso share it is desirable to identify at the earliest possible stage whether other shares in the same property are already registered in the Land Register. If they are, the interest will be added to the title sheet for the existing registered shares. The proportion conveyed, as entered in the proprietorship section, should reflect the terms of the deed, i.e. the entry should be in the same format (percentages or fractions) as in the deed being registered.

It is preferable for all interests in a plot of land to be registered at the same time, however there is no statutory requirement to do so with transitional arrangements permitting the title sheet to be built up over time.

In the event that registration of the whole interest is not possible (whether because the other shares are owned by a third party, or because the applicant declines to apply for voluntary registration), the legal registration officer will deal with the application according to the procedure outlined in the following paragraphs.

Title sheet

A single title sheet is created and maintained for each whole unit of property; as additional shares are registered, they will be added to this title sheet.

Property section

The plans registration officer will map the subjects by the most convenient method, but the verbal description in the property section will describe the subjects as a whole unit. The fact that the title relates only to a pro indiviso share will be covered in a note, e.g.:

Subjects cadastral unit REN15243 being 31 RENFREW ROAD, NEWTON MEARNS edged red on the cadastral map.

Note: The above property is registered in this title only as regards the total of shares shown in the proprietorship section.

This style is used so that no change to the property section is required when further shares are added to the title sheet. When all the shares have been registered (i.e. the total share registered equals one or 100%), the note should be removed.

The "date of first registration" noted in the property section, will be the date of registration of the first share. No further dates should be added when further shares are registered. See examples below:

The proportion conveyed, as entered in the proprietorship section, should reflect the terms of the deed, i.e. the entry should be in the same format (percentages or fractions) as in the deed being registered. If the deed being registered appears to convey a larger proportion of the subjects than the share that the granter is entitled to (for example, 1/3 is larger than 33%) the case should be referred to a senior caseworker.

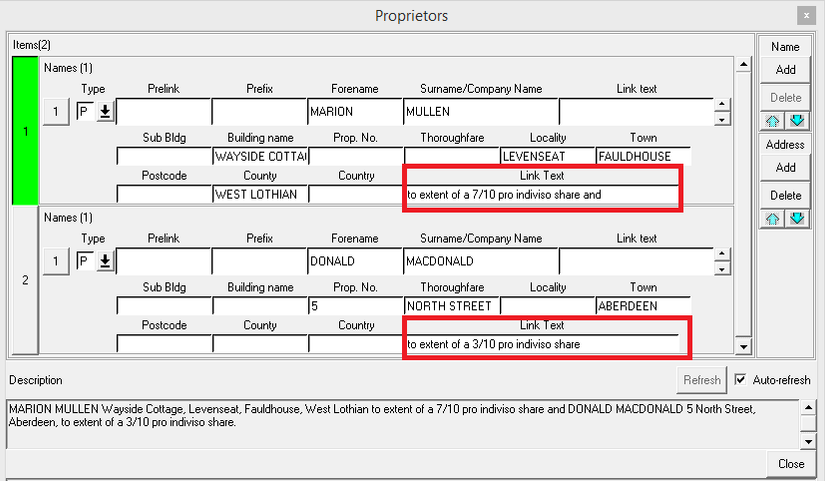

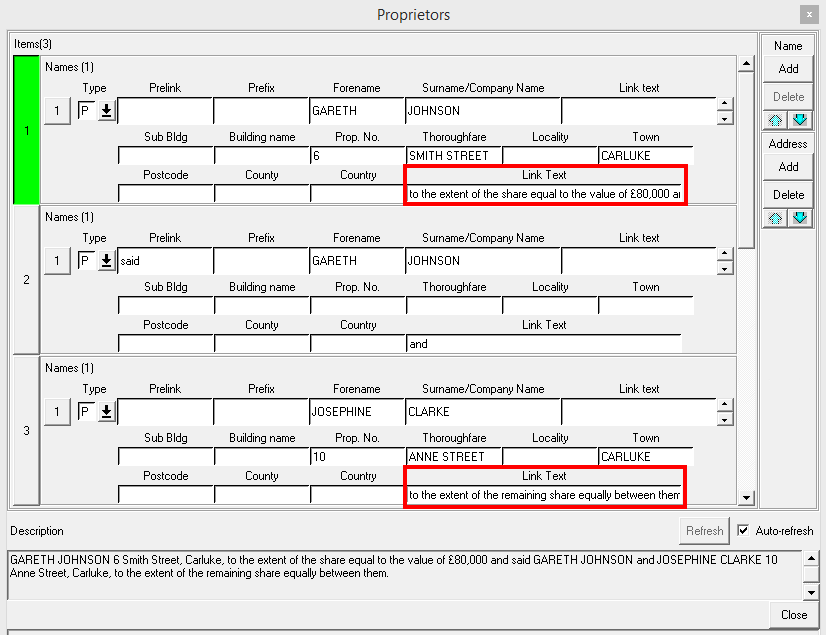

When different shares are conveyed in a single deed, the details must be entered in the Link Text and not the Extra Description box to allow the LRS to show the position correctly, see below.

Example 1:

Example 2:

If the pro indiviso shares exceed one or 100%, including the share the registration officer is dealing with, a referral must be made to a senior caseworker. The registrable deed may not be valid and the application may require to be rejected.

Joint Ownership

In joint ownership, unlike ownership in common, none of the owners has a right in the property which he/she acting alone can alienate to another. The right of a joint owner falls (or accresces) to the other joint owners on death - the right of a joint owner cannot be alienated or disponed of by that owner either during their lifetime or on their death.

The most commonly encountered type of joint ownership is where a property is owned by proprietors acting in a trust capacity - for example trustees acting under a trust or for a firm, club, unincorporated association or religious organisation, or as joint Executors.

For styles of designation of proprietors in a trust capacity, see Designations

In the case of joint ownership, the deed will not contain a statement about the respective shares of the proprietors in their trust capacity.

Other Information in the Proprietorship Section

In addition to the information that falls to be entered in the proprietorship section in terms of section 7 of the 2012 Act, the Keeper can also add such other information as considered appropriate. This section contains details of such further information.

Entry number

The entry number will be inserted in the first column of the proprietorship section. The need to use more than one entry will arise when co-proprietors and parties holding separate pro indiviso shares register their respective interests by separate deeds or applications - for styles see Common ownership examples above.

Date of registration

By section 37 of the 2012 Act, the date of acceptance of an application by the Keeper becomes the date of registration. Where there is more than one entry in the proprietorship section, the entries will be inserted in date order.

For special cases see examples below:

Consideration

In terms of regulation 12(2)(a) of the Rules, the proprietorship section must contain the consideration for the deed(s) by which the proprietors were entered in the title sheet. The consideration stated in the deed should be accurately reflected in the title sheet. Where the deed narrates that the total price has been paid by the parties 'equally', and the dispositive clause narrates that the property is conveyed to them 'equally' (or 'equally and to the survivor'), only the sum of money paid should be reflected in the 'consideration' field. The price can be carried forward on the LRS from the application workdesk, but there will be occasions where the officer will need to amend the entry.

The requirement in the 2012 Act is that an application should provide the Keeper with the information required to complete the title sheet. Where there is no consideration stated in a deed, but there is a monetary consideration stated in the application form, then the title sheet can be completed from the information given in the application form.

A deed should not be rejected because the consideration has been left out of the deed, where it has been stated as a Monetary consideration in the application form.

The Value field of the application form should not be used to complete the consideration in the title sheet.

Date of entry

In terms of Regulation 12(2)(b) of the Rules, the proprietorship section of a title sheet must contain the date of entry. The entry date given in a deed is the date when, in exchange for payment of any monetary or other consideration, the acquirer takes possession of a property.

The date of entry should be entered in the same format as the date of registration, i.e. dd mmm yyyy. The various phrases in the deed that accompany the date of entry (e.g. ‘and actual occupation’) should be omitted.

Where the DIR states that entry takes effect from the 'date hereof', the date to be entered in the proprietorship section is the last date of execution of the deed.

Registers of Scotland (RoS) seeks to ensure that the information published in the 2012 Act Registration Manual is up to date and accurate but it may be amended from time to time.

The Manual is an internal document intended for RoS staff only. The information in the Manual does not constitute legal or professional advice and RoS cannot accept any liability for actions arising from its use.

Using this website requires you to accept cookies. More information on cookies.

Feedback